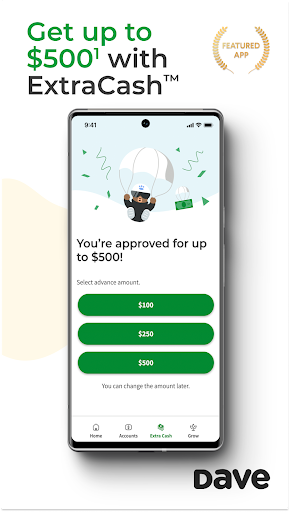

Dave - Up to 500 in 5 mins

Dave, Inc

Editor's summary

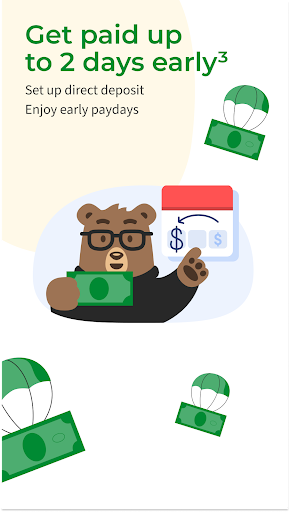

One-line summary Dave is one of the more practical cash-advance apps because it’s fast, relatively straightforward, and doesn’t feel overly predatory, but it’s still a short-term money tool that only really shines if your income and repayment pattern fit its system.

-

Installs

10M+

-

Developer

Dave, Inc

-

Category

Finance

-

Content Rating

Everyone

-

Latest version

3.52.0

-

Package

com.dave

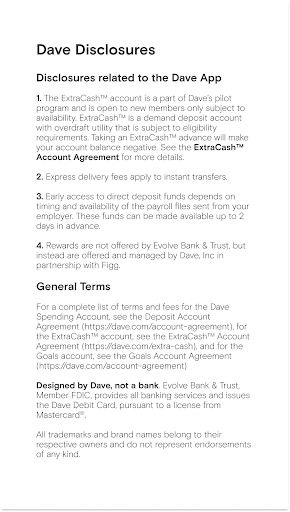

Screenshots

In-depth review

Recommended Apps

-

Office Word Reader: PDF, DOCX

iKame Applications - Begamob Global4.7

-

7-Eleven: Rewards & Shopping

7-Eleven, Inc.4.8

-

Flip Diving

MotionVolt Games Ltd4.4

-

Maps, Navigation & Directions

Universal Nav4.1

-

Kismia - Meet Singles Nearby

Kismia Group4.1

-

Popsicle Stack

Lion Studios4.3

-

BCBSIL

Blue Cross and Blue Shield of Illinois3.1

-

Bigo Live - Live Streaming App

Bigo Technology Pte. Ltd.4.5

-

Aura: Meditation & Sleep

Aura Health - Mindfulness, Sleep, Meditations4.5

-

Talkatone: Texting & Calling

Talkatone, Llc4.0

-

FTX: Buy & Sell Crypto

Blockfolio, Inc4.0

-

Plex: Find Movies & TV Shows

Plex, Inc.3.7

-

Roblox

Roblox Corporation4.3

-

Intune Company Portal

Microsoft Corporation2.9

-

Apple Music

Apple4.6

You May Like

-

GoFundMe: Fundraise and Give

GoFundMe Inc4.7

-

Splitwise

Splitwise4.3

-

Discover Mobile

Discover Financial Services4.7

-

Experian

Experian4.7

-

MetaMask - Blockchain Wallet

MetaMask Web3 Wallet4.5

-

Trust: Crypto & Bitcoin Wallet

DApps Platform, Inc.4.5

-

Fidelity Investments

Fidelity Investments4.2

-

Bitget - Buy & Sell Crypto

BG LIMITED4.0

-

GEICO Mobile - Car Insurance

GEICO Insurance4.6

-

SuperQi

THE INTERNATIONAL SMART CARD CO.LLC1.1

-

Venmo

Venmo4.1

-

Propel EBT & SNAP Benefits

Propel Inc4.8

-

Freecash: Earn Rewards

Freecash4.5

-

OnePay – Mobile Banking

ONE Finance, Inc.4.8

-

PhonePe UPI, Payment, Recharge

PhonePe4.3