SuperQi

THE INTERNATIONAL SMART CARD CO.LLC

Editor's summary

One-line summary SuperQi is appealing as a genuine all-in-one wallet for everyday payments and account access in Iraq, but I’d hesitate to recommend it because reliability problems quickly overshadow the convenience.

-

Installs

10M+

-

Developer

THE INTERNATIONAL SMART CARD CO.LLC

-

Category

Finance

-

Content Rating

Everyone

-

Latest version

1.0.44

-

Package

iq.qicard.qipay.prod

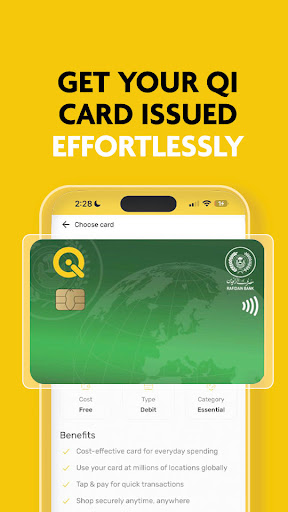

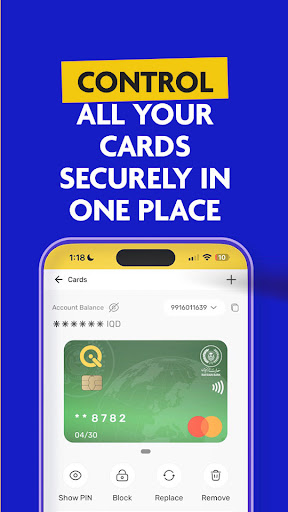

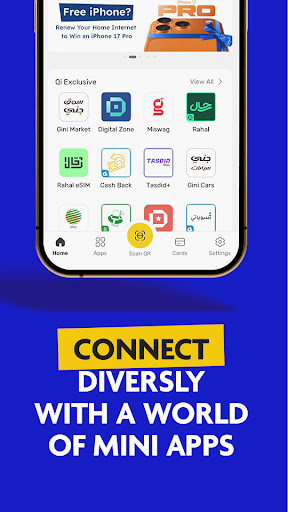

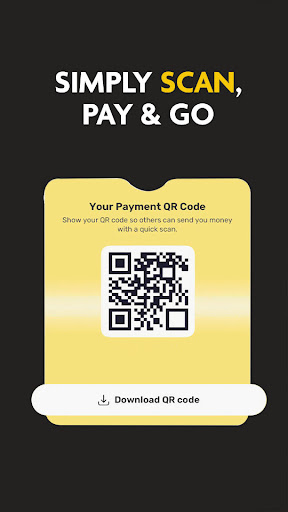

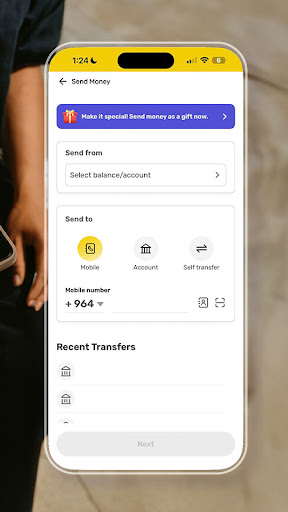

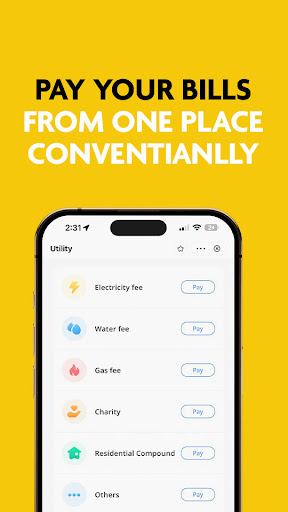

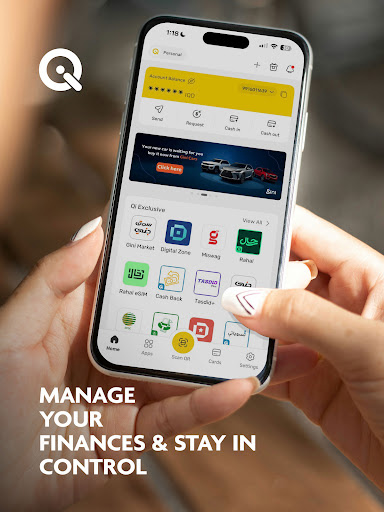

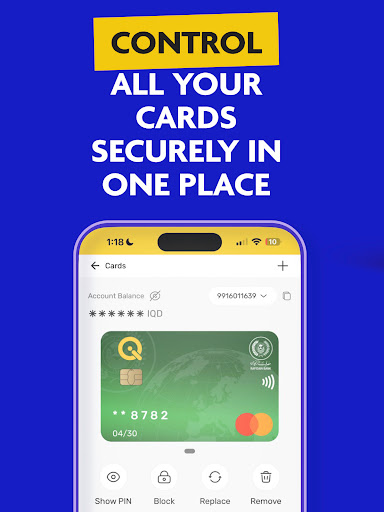

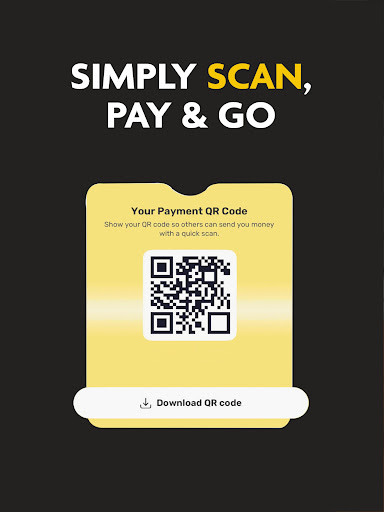

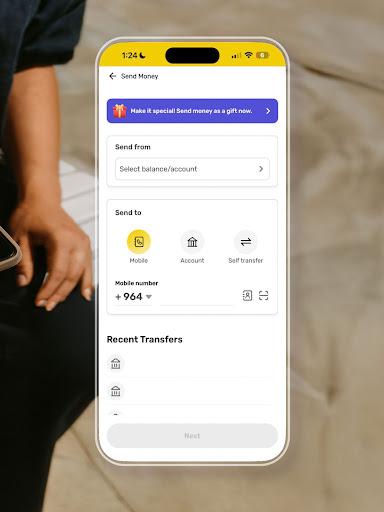

Screenshots

In-depth review

Alternative apps

- Zain Cash

- AsiaHawala

- urpay

Recommended Apps

-

Genshin Impact

COGNOSPHERE PTE. LTD.4.1

-

PDF Reader - All PDF Scanner

Dev Globeg4.6

-

Zedge™ Wallpapers & Ringtones

Zedge4.7

-

SCHOOLBOY RUNAWAY - STEALTH

Linked Squad4.0

-

Plants vs. Zombies™ 2

ELECTRONIC ARTS4.2

-

Piano Game: Classic Music Song

Dream Tiles Piano Game Studio4.3

-

Hey Color Paint by Number Art

ZephyrMobile4.6

-

Ellume COVID-19 Home Test

Ellume Limited1.4

-

Beatstar - Touch Your Music

Space Ape4.6

-

Jump into the Plane

BoomBit Games4.2

-

Bob's World - Super Run Game

OneSoft Global PTE. LTD.4.5

-

Talking Tom & Ben News

Outfit7 Limited4.5

-

The Grand Mafia

YOTTA GAMES4.3

-

Labcorp | Patient

Laboratory Corporation of America Holdings/LabCorp3.1

-

Samsung Members

Samsung Electronics Co., Ltd.4.6

You May Like

-

Capitec Bank

Capitec Bank4.0

-

Klarna: Smarter everyday money

Klarna Bank AB (publ)4.8

-

Brigit: Cash Advance & Credit

Brigit4.8

-

MyBlock

H&R Block4.0

-

Fidelity Investments

Fidelity Investments4.2

-

Bitget Wallet: Crypto and BTC

Bitget Wallet4.7

-

Testerup: Test & Earn Rewards

aestimium GmbH4.3

-

TradingView: Track All Markets

TradingView Inc.4.7

-

KuCoin: BTC, Crypto Exchange

Kucoin Technology Co., Ltd.4.4

-

JPay

Jpay Mobile4.1

-

Wise

Wise, formerly TransferWise4.2

-

Discover Mobile

Discover Financial Services4.7

-

MetaMask - Blockchain Wallet

MetaMask Web3 Wallet4.5

-

OPay

OPay Digital Services Limited4.6

-

Experian

Experian4.7