Intuit Credit Karma

Credit Karma, LLC

Editor's summary

One-line summary Credit Karma is one of the easiest free ways to stay on top of your credit and finances, but if you hate product recommendations woven into the experience, its constant offers can feel like the price of admission.

-

Installs

50M+

-

Developer

Credit Karma, LLC

-

Category

Finance

-

Content Rating

Everyone

-

Latest version

26.10.1

-

Package

com.creditkarma.mobile

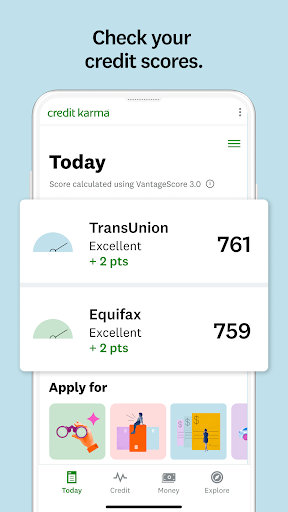

Screenshots

In-depth review

Alternative apps

Recommended Apps

-

Stocard - Rewards Cards Wallet

Stocard4.5

-

Train Station 2: Train Games

Pixel Federation Games4.3

-

Dancing Cats 2: Music Games

Cobby Labs4.4

-

Perfect Piano

Revontulet Soft Inc4.2

-

1945 Air Force: Airplane games

ONESOFT GLOBAL PTE LTD4.8

-

Randonautica

Randonauts Co.3.1

-

Google Calendar

Google LLC4.2

-

Video&Drama Player All Format

Griffin Atlas USA3.5

-

FTX: Buy & Sell Crypto

Blockfolio, Inc4.0

-

QR & Barcode Scanner

Gamma Play4.8

-

Ultimate Car Driving Simulator

Sir Studios4.1

-

Music Player &MP3- Lark Player

Lark Player Studio4.6

-

Pizza Hut - Delivery & Takeout

Pizza Hut Inc3.8

-

Hair Dye

CrazyLabs LTD4.2

-

Fruit Ninja®

Halfbrick Studios4.5

You May Like

-

IRS2Go

Internal Revenue Service4.0

-

GEICO Mobile - Car Insurance

GEICO Insurance4.6

-

Mint: Budget & Track Bills

Intuit Inc4.3

-

Google Wallet

Google LLC4.4

-

Green Dot - Mobile Banking

Green Dot4.0

-

PayPal - Pay, Send, Save

PayPal Mobile4.2

-

Tonkeeper — TON Wallet

Ton Apps Limited4.6

-

JPay

Jpay Mobile4.1

-

Allstate Mobile

Allstate Insurance Co.3.9

-

CNBC: Business & Stock News

NBCUniversal Media, LLC4.5

-

Venmo

Venmo4.1

-

SuperQi

THE INTERNATIONAL SMART CARD CO.LLC1.1

-

MyBlock

H&R Block4.0

-

Wise

Wise, formerly TransferWise4.2

-

PayMe - Claim Your Money

Prove It4.8