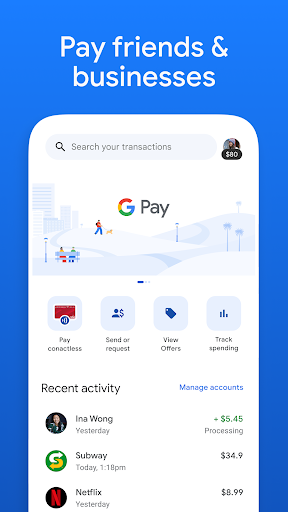

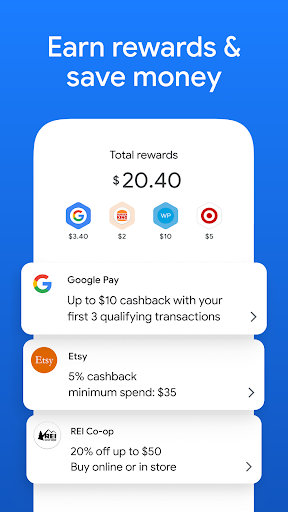

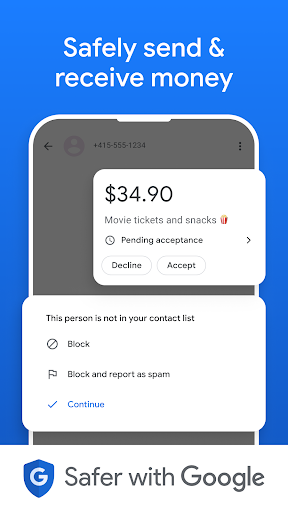

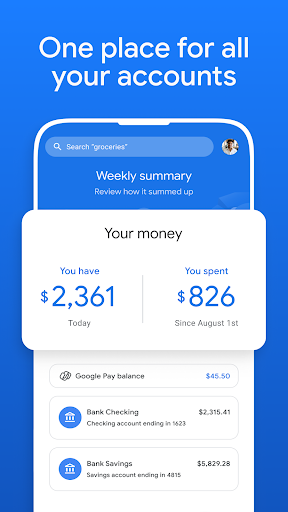

Google Pay: Save and Pay

Google LLC

Editor's summary

One-line summary Google Pay still feels fast, familiar, and trustworthy for everyday payments, but it is hard to recommend this listing when the U.S. standalone app is no longer usable and the experience now depends heavily on what region and workflow you need.

-

Installs

1B+

-

Developer

Google LLC

-

Category

Finance

-

Content Rating

Everyone

-

Latest version

VARY

-

Package

com.google.android.apps.nbu.paisa.user

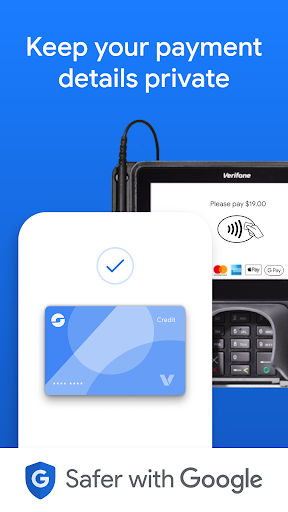

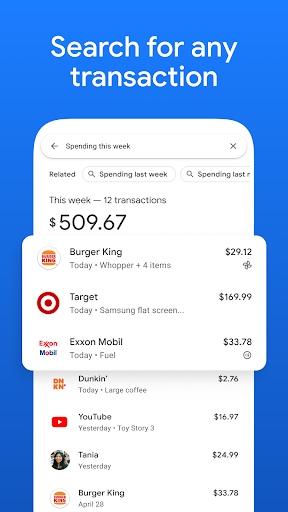

Screenshots

In-depth review

Alternative apps

Recommended Apps

-

Mafia City

YOTTA GAMES4.5

-

Ant Legion: For The Swarm

37GAMES4.6

-

Google Play Games

Google LLC4.3

-

Bodybuilder GYM Fighting Game

Fighting Arena4.7

-

Ball Run 2048: merge number

KAYAC Inc.4.2

-

Lamar - Idle Vlogger

CrazyLabs LTD4.3

-

Chipotle

Chipotle Mexican Grill4.7

-

Square Point of Sale: Payment

Block, Inc.4.8

-

Dairy Queen® Food & Treats

International Dairy Queen®️4.4

-

Depop - Buy & Sell Clothes App

Depop4.7

-

Rocket Money - Bills & Budgets

Rocket Money - Bills & Budgets4.6

-

Safe Cleanup - Cleaner&Booster

Surf tool4.1

-

SEGA FOOTBALL CLUB CHAMPIONS

SEGA CORPORATION4.6

-

Intelligent Hub

VMware Workspace ONE3.0

-

AI Chat - Ask your AI Chatbot

Syphnosys Apps4.4

You May Like

-

Testerup: Test & Earn Rewards

aestimium GmbH4.3

-

Bitget - Buy & Sell Crypto

BG LIMITED4.0

-

Mint: Budget & Track Bills

Intuit Inc4.3

-

Brigit: Cash Advance & Credit

Brigit4.8

-

Tonkeeper — TON Wallet

Ton Apps Limited4.6

-

Paysend: Simple Money Transfer

Paysend Technology Limited4.7

-

Discover Mobile

Discover Financial Services4.7

-

Green Dot - Mobile Banking

Green Dot4.0

-

State Farm®

State Farm Insurance4.6

-

Venmo

Venmo4.1

-

KuCoin: BTC, Crypto Exchange

Kucoin Technology Co., Ltd.4.4

-

Stash: Investing made easy

Stash Financial4.0

-

Experian

Experian4.7

-

Intuit Credit Karma

Credit Karma, LLC4.7

-

Binance: Buy Bitcoin & Crypto

Binance Inc.4.6